We have been asked many times about the process of getting a mortgage in Spain. Whether that is in regard to Valencia or any other parts of Spain it's essentially a standard process. However, it may not be like the process of applying for and getting a mortgage in other countries so today we are looking at the process of getting a Spanish mortgage from start to finish.

The Choices

There are essentially two ways to go to start looking for a mortgage in Spain; the bank or the broker. Both are valid ways to go and in the end they will cost you a similar amount. There are fees of course when using a broker but you will often find that they are able to negotiate you a better deal with the bank and that those discounts they get for you offset the fee.

The Bank Route

You may already have a bank account in Spain and the natural thing to do in those circumstances is to walk into your bank and ask them about their mortgages.

That may well be your first mistake. If the bank know they already hold you hostage they will definitely not offer you the best conditions. You could also walk into a few banks but as the others don't know you then you might well find that getting a mortgage with them is difficult, more hoops to jump through than with your own bank, and that the conditions they offer you are not great. It's not as easy as it looks on the following image.

The Broker Route

Mortgage brokers in Spain are a growing industry. For many years it was a bit of a wild west industry but the professionalisation of the industry has been remarkable since the bad old days prior to the financial crash of 2008.

The best brokers work with all of the banks in Spain to find you the best mortgage deal for you personally. They are able to offer mortgage deals for people who are self employed, non residents, mortgages on rustic properties and more standard mortgages too of course. The terms and conditions for each of these situations will be different. Maximum loan to value is different for residents and non residents, approval may be denied if your income is in a weaker currency and many other individual situations turn up that mean it is important to take the next step of the pre-approval before proceeding.

However, you can often get an idea of what you are likely to be offered by a mortgage broker. We work closely with Mortgage Direct for example in Valencia and the rest of Spain and we have written about Mortgage Direct and their services previously in the blog.

The Pre-Approval

This is very important if you are not sure about your suitability for a mortgage. Getting a preapproval on your mortgage essentially means that you get an idea as to whether you are likely to be approved for your mortgage before you start to put any money down. In order to get a pre-approval bear in mind that you will need to provide a lot of the paperwork that you will need for your actual mortgage application, income statements, tax returns, other income streams etc...

The broker or bank will look at your papers and give you an in principle yes, no or maybe and perhaps more importantly an idea about how much you are likely to be able to borrow. This is very important because what you don't want to do is overestimate two things, firstly what price range you are going to be searching for a property in and secondly the percentage that the bank is likely to offer you based on the valuation or price of the property.

This second issue is very important due to changes in the way banks lend since the financial crisis. Let's assume that the bank is willing to give you 70% Loan to Value (LTV) ratio. The LTV ratio is based on one of two things, the price you are paying or the valuation of the property. It used to be the case that the bank would give you 70% of the higher of the two values. Now they will give you 70% of the lower of the two values. This makes a significant difference especially if the valuer decides to value the property lower than the asking price which often happens. The reverse can happen too that they value significantly higher but even then the mortgage gets based on the sale price!

If a bank isn't too interested in you as a potential mortgage holder they will instruct the valuer to be harsh in their valuation. (They aren't supposed to do this but what banks are and are not supposed to do compared to what they actually do is a moot point.)

The Property

Now the easy part, you need to find a property. Knowing your limits by having a pre-approval from the bank can help you enormously at this point because it stops you looking at properties that are way out of your price range. However bear one thing in mind, your costs of purchase are not taken into consideration wither by the valuer or the bank. If the bank has offered you 70% then you will need to find 45% of the total price as a minimum, the 30% remaining of the cost price of the property and the estimated 15% costs for purchasing a property. (10% tax, 3% agency fees, 1% notary and registry fees and 1% legal fees because you should be using a lawyer for your purchase.) As an example, a property at 200,000 Euros really costs you 230,000 with taxes and costs. If you are offered 70% then you will get 140,000 Euros from the bank meaning you will have to find 60,000 for the purchase and 30,000 for the costs, a total of 90,000 euros.

Equally, if the valuation is low, let's say 180,000 euros, then you will only get 126,000 Euros meaning you have to find a total of 74,000 for the purchase plus 30,000 Euros for the costs.

The Valuation

The valuer requires some paperwork from you. This year they ask for another piece of paper that previously wasn't required, which is the "first occupation licence". You should get this too if you are not getting a mortgage but most sales this year so far have not had it as the buyer can defer from insisting on it at the notary and most people either can't find it or haven't got a recent one and town halls may take ages to get one. With a mortgage though the bank may insist.

The valuer also asks for a copy of the deeds, a Nota Simple from the property registry, a document from the town hall to state there are no infractions on the property and potentially other papers depending on the property. These are things that your lawyer may already have at this point but you ask for them from the owner if you don't have them.

The Mortgage Study

At the same time as the valuation you should be delivering any outstanding paperwork to your bank or broker for the study of your case for a mortgage. In the pre-approval stage you will have delivered the basics so that the bank or broker can give you an in principle "yes". Now is the time to gather up your tax returns from the last three years, scrape together proof of income through salary slips, bank statements to confirm those salary payments, rental income, dividend payments etc...

The bank will look at your outgoings at this point too and also your current indebtedness. Remember that rental income on properties is often offset to a great extent by mortgage payments on that property. It's a good idea to lower your outgoings in the few months up to applying for a mortgage to show that your affordability criteria is valid.

The Affordability Criteria

The question the banks are asking themselves through this process is whether you can afford to pay the mortgage when you get it. As a rule of thumb use 33% of income for affordability. What does that mean?

If you earn 2400 Euros per month then expect the bank to be ok with a monthly repayment of around 800 Euros assuming you are not bogged down with regular debt payments such as car loans, credit cards etc... Also if you can show that you are currently paying a certain amount on a property in rental and this will convert into your mortgage payment and that you have been regularly paying that amount for years without any problem then that is helpful for your case.

The Approval

Eventually the bank will approve you for the mortgage under certain terms and conditions and make you an offer based on that approval. There are certain terms that are more important than others but the basics are as follows: the mortgage period, the interest rate, the type of interest charged and the monthly payment amount.

Let's take them one by one.

Firstly the time period. Mortgages in Spain have an average life span of around 23 years the last time I read about it. It is normal to be given a mortgage for 20, 25 or 30 years with some banks going to 35 years with an upper age limit of 75 or even 80 years old at the end of the mortgage term. However with interest rates being so low currently and the trend being for fixed rate mortgages, banks are often looking at 20 year fixed interest mortgages. If you get a good fixed rate interest mortgage then take it, as our American clients say, "2% fixed rate for 20 years!!!??? Free money!"

And on that interest rate, our latest mortgage approvals have been anything from 1.5% fixed rate to 2.75% fixed rate. Why the variability? It depends on the client profile, the source of funds, the inherent risk etc...

Basically, if you don't need the money then the bank will give you a better rate of course, go figure!

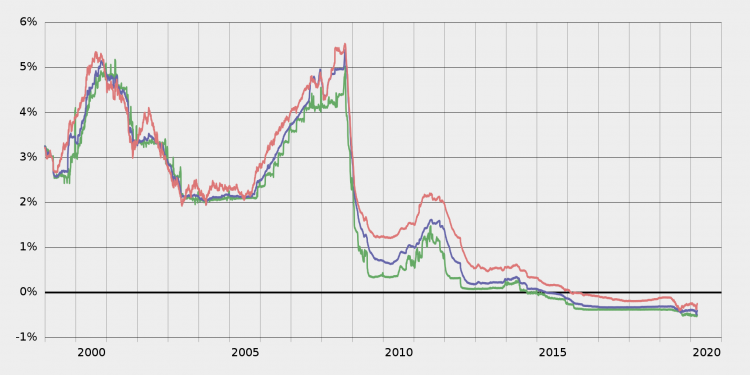

If you get a variable rate then expect first year rates of around 1.25% and upwards and ongoing rates, they change every year according to the base Euribor rate, of anything from Euribor +0.8% upwards. As Euribor is currently in negative territory it might seem a good idea but if the rate rises in the future your payments on the mortgage could rise every year, remember that Euribor in 2008 was as high as 5.6% before the financial crisis.

The monthly payment is made up of two parts, the capital repayment and the interest payment. On your bank account it will show as a single payment but it is two separate parts. On signing for the mortgage the bank will give you a printout of the payments you will make either over the first year in the case of variable rate mortgages or for the life of the mortgage in the case of fixed rate mortgages and this will detail how much of the whole payment is capital and how much interest.

The Costs

Until a couple of years ago it was quite expensive to get a Spanish mortgage, it could add anything from 2% to 4% onto the purchase costs of the property. Then the courts ruled that the eventual beneficiary of any mortgage is the bank itself as the property reverts to their ownership if you as a mortgage taker don't pay them. Therefore they have to pay the majority of the costs of a mortgage now and those costs include the tax on a mortgage and the paperwork and the notary and registry costs. Now you only have to pay the valuation in advance, which many times they will refund, an opening commission and maybe a study fee.

A broker will charge you a fee for their services but it is likely that they will be able to get you a better deal than you would get yourself at a bank as they play off your mortgage requirements with others and the banks make offers to them based on your profile. Therefore it is highly recommended to look through a broker rather than just walking in off the street to a bank, especially if you are not a fluent Spanish speaker, as the bank will try to get one over on you, that's what they do!

The Paperwork

Once you are approved and the valuation has been submitted the bank make you an offer and at this point somebody goes out from the bank with a chainsaw and chops down half of the nearest forest to provide you with the paperwork you will have to sign in duplicate or triplicate.

The paperwork will detail the interest rate, the time period of the mortgage, the monthly payment, details of the value the bank place on the property, any bonuses the bank apply to your initial mortgage rate (Depositing salary into the bank, placing direct debits through the bank, taking the bank's insurance etc...) details of how much the bank will sell the property for if you default, the steps they will take before repossessing in case of non payment,

And it is now when it begins to get interesting. Because at this point you become an expert on mortgages in Spain because you need to make your first visit to the notary to sign the mortgage. And most notaries like to show off if they are at a loose end.

The Notary for the Mortgage

Ten days before you can sign for the purchase the mortgage is sent to your chosen notary. The countdown starts to your purchase at this point. You have to go to the notary so they can read you the conditions of the mortgage and perhaps a few other things.

Last week I had two mortgage signings prior to purchases in which I acted as a translator for the clients. So at this point I take a breath...

One time it took over an hour and a half because the notary wanted to demonstrate his undoubted knowledge about...

"what mortgages are, the finer details of the history of mortgages on properties, the difference between the Australian daily rate of interest and the European method (The clients weren't Australian) what happens if you don't pay the mortgage, the potential scenarios about why you might not pay the mortgage, the potential changes of interest rate if you are late with payments, what the bank will do to you if you don't pay which may or may not have included thumbscrews and being thrown in the stocks, how much they will sell your property for if they take it from you, why you will still owe the bank money if they did that and how the bank will own you for the rest of time if, god forbid, any of this came to pass. There may have been the actual financial details of the mortgage too but I was on translation autopilot by that time. The clients then had to complete a quiz to show that they had understood the terms and conditions of their mortgage so I had to translate that as well and then they both signed declarations to the effect that they had been battered into submission and they understood the implications and repercussions."

The other took ten minutes, the notary was in a rush and just asked them to sign off on the quiz after mentioning the financial conditions of the mortgage. He then went for a coffee with a mate!

Why is this done? Previously you signed for the mortgage and on continuation signed for the house in the same room on the same day. Banks were notorious for slipping in extra charges, potentially illegal contract terms and doing other slippery weasel type things so the government introduced a ten day cooling off period for anyone feeling that they were railroaded into signing their mortgage.

The Notary For The Purchase

After you have signed for the mortgage then you sign for the property at the notaries but not before ten days have elapsed from when the notary received the initial mortgage documents. At this point the mortgage is read again and the "Gestor" from the bank will make sure the conditions in the mortgage deed match those sent ten days before. Then you read the purchase document, sign the deed, swap the keys for the cheques and the house is yours...

Hold on... what do you mean "cheques". Well, the bank or your lawyer or you will bring along a bank draft to pay the difference between the total price and what you have already paid as a deposit. This amount may be made up of one cheque (Bank Draft) or many. There may be one to cancel a current mortgage made out to another bank, one to cancel other debts on the property and a few to give each seller a cheque for their stipulated amount, this often happens with inheritances for example.

The reason that this is done in bank drafts and not in cash, bank transfer or even Bitcoin or bartering is because everyone recognises that a bank draft is "good money" and the banks want to keep their monopoly on these payments so they can charge a lot of money for the simple service of printing out a cheque or two.

The Payments

After the signing you have to start paying the bank back their money of course. This is usually done between the first and the fifth of the month via direct debit from your bank account. If you haven't got the money in the account the bank will charge you between 18 and 30 Euros for the privilege of sending you a letter, yes, a letter, (as opposed to sending you a text message or a mail to let you know immediately) to tell you that you haven't paid them and they will start charging a higher interest rate on your mortgage for the days until you get up to date on payments, usually 2 or 3% above your normal rate.

The Cancellation

You can partially or fully cancel a mortgage by making a payment into your mortgage account. If you suddenly win the lottery and decide to pay off the mortgage you can deposit money into the account to cancel the mortgage and the bank will arrange for you to go to the notary again to cancel the mortgage against the property and in the property registry. However it is more likely that you make a partial payment to cancel a part of the mortgage and bring the total amount down. You might come into some money through an investment, an inheritance or by selling a car or something and decide to partially cancel your mortgage. When you do you are given the choice to reduce the monthly amount or reduce the time period of the mortgage.

Cancelling a mortgage totally will often cost you money both in a commission, which the notary will have detailed to you in your initial interminable notary meeting, and for the final paperwork and registry cancellation. Cancelling partially may cost you for example half of one percent of the amount cancelled but it is detailed again in the conditions of the mortgage.

Clear Enough?

This was written as a thorough guide to the process for getting mortgages in Spain as we get asked the question constantly by our clients. Now I can just point them to this post and then point them towards our homepage to choose their property. If you have enjoyed this or even just made it to the end because you realise that this is something you should know then feel free to share it to your friends and social contacts. We appreciate every share to get the word out as it helps me to not have to explain it again ;-)

If you liked this...

Then make sure to go to our essential reading page here or by clicking on the image below or directly to some of our other most popular articles below too.